What Is Inventory? Definition, Types, & Examples

- mark599704

- Nov 22, 2023

- 11 min read

Updated: Aug 21, 2025

Inventory Definition

Inventory refers to all the items, goods, merchandise, and materials held by a business for selling in the market to earn a profit.

Example: If a furniture store purchases wood to manufacture tables, the wood and finished tables will be considered inventory. However, the machinery used to cut and assemble the wood will be treated as an asset.

Inventory As Noun

Inventory is a complete list of items such as property, goods in stock, or the contents of a building.

Inventory As Verb

Make a complete list of.

Inventory Pronunciation

in·vuhn·taw·ree

in·ven·to·ry

/ˈinvənˌtôrē/

Usage Examples Of Word Inventory

"The bookstore keeps a vast inventory of classic and contemporary literature across all genres."

"Due to supply chain delays, the company decided to increase its inventory of essential components."

"Our inventory of spare parts is updated weekly to ensure smooth operations in the repair center."

"Each item in the museum’s inventory has been carefully cataloged and preserved for research purposes."

"They conducted a full inventory before the annual audit to verify stock levels."

"The fashion retailer rotates its inventory every season to keep up with changing trends."

"Our warehouse inventory includes everything from raw materials to finished goods ready for shipment."

Similar Words / Synonyms for “Inventory”

List

Listing

Catalog

Directory

Record

Register

Checklist

Tally

Roster

File

Log

Account

Archive

Description

Statement

Videos Related To "What Is Inventory?"

Inventory refers to a company's goods and products that are ready to sell, along with the raw materials that are used to produce them.

Inventory, also known as stock, is a crucial aspect of any business operation. Inventory can include raw materials, work-in-progress items, and finished goods. In this article, we will define inventory and explore its various types. We will also give examples for each type and discuss why inventory control and management are important.

Related Blogs:

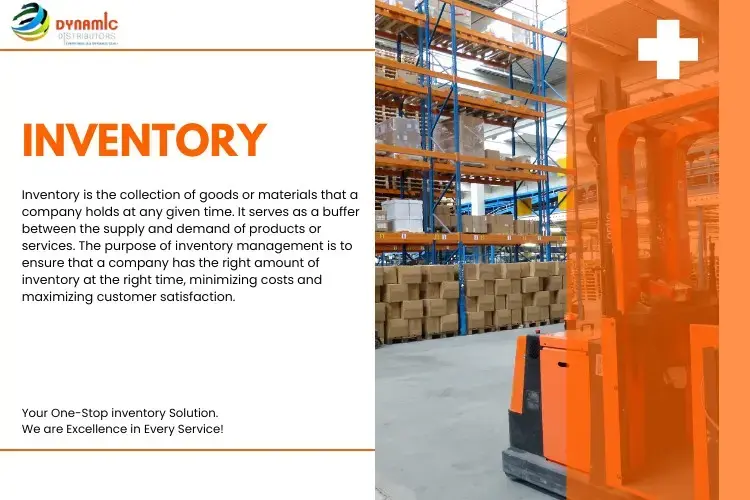

What is Inventory?

Inventory is the collection of goods or materials that a company holds at any given time. It serves as a buffer between the supply and demand of products or services. By maintaining inventory, businesses can meet customer demands promptly and maintain a smooth production process. Inventory can be classified into various types, each with its unique characteristics.

Key Takeaways of Inventory

Asset Classification: Inventory is a current asset on a company's balance sheet. It includes the raw materials used in production and the finished goods available for sale.

Valuation Methods: Inventory is valued using different methods, such as first-in, first-out (FIFO), last-in, first-out (LIFO), and weighted average. These methods impact how the cost of goods is accounted for in financial records.

Cost Management: Efficient inventory management helps businesses control costs. It ensures that goods are produced or acquired only as needed, which prevents excess inventory and avoids higher holding costs.

Operational Flexibility: Inventory management allows businesses to adjust production or purchasing based on demand. This helps balance supply with customer needs.

Inventory Valuation Methods

Inventory can be valued in three ways. Here are inventory valuation methods:

First-In, First-Out Method (FIFO): In FIFO, inventory valuation follows the principle of using the oldest items first. Items added to the inventory earliest are presumed to be the first ones sold or utilized in the production process.

Last-In, First-Out Method (LIFO): LIFO means that the newest items added to the inventory are the first to be sold or used. This is the opposite of FIFO.

Weighted Average Method: The weighted average method calculates the average cost of all inventory units. It combines the cost of new items with the cost of existing inventory to give a blended cost per unit.

Types of Inventory

The types of inventory are the following:

Raw Materials: These are the basic materials used in manufacturing processes. They include metals, plastics, fabrics, and chemicals, among others.

Work-in-Progress: Work-in-progress inventory consists of partially completed products that are still undergoing manufacturing processes.

Finished Goods: These are the final products that are ready for sale or distribution to the end customer.

Maintenance, Repair, and Operations (MRO) Inventory: MRO inventory consists of items required to maintain and repair equipment, machinery, and facilities.

Transit Inventory: Transit inventory refers to goods that are moving between different locations. This includes items traveling between warehouses or distribution centers.

Cycle Inventory: Cycle inventory represents the stock of goods that varies with the regular replenishment cycles of a company.

Anticipation Inventory: This type of inventory is held in anticipation of future demand. It is often used for seasonal or promotional purposes.

Safety Stock: Safety stock is extra inventory kept to avoid running out of stock. It helps manage unexpected changes in demand or supply.

Buffer Inventory: Buffer inventory is maintained to protect against uncertainties in demand, supply, or lead times.

Obsolete Inventory: Obsolete inventory refers to items that are no longer in demand or have become outdated. It is important to dispose of obsolete inventory to free up storage space and avoid losses.

Consignment Inventory: Consignment inventory is held by a retailer but is owned by the supplier. The supplier retains ownership until the goods are sold.

Excess Inventory: A retail store ordered more units of a seasonal product than customers wanted. This resulted in unsold items left over after the season.

Decoupling inventory: Decoupling inventory is stock placed in the production process. It helps buffer against disruptions and ensures a smooth workflow.

Theoretical inventory: Theoretical inventory represents an idealized stock level, calculated to meet demand without overstocking or causing delays.

Example Of Types Of Inventory

To better understand the different types of inventory, let's consider some examples:

Raw Materials: A furniture manufacturer holds various types of wood, fabric, and screws as raw materials.

Work-in-Progress: An automobile manufacturer has partially assembled cars on the production line.

Finished Goods: A clothing retailer has a stock of finished garments ready for sale.

MRO Inventory: A maintenance department holds spare parts, tools, and lubricants for equipment maintenance.

Transit Inventory: A wholesaler has goods being transported from the manufacturer to their warehouse.

Cycle Inventory: A grocery store maintains a regular stock of perishable and non-perishable goods.

Anticipation Inventory: A toy manufacturer increases production in preparation for the holiday season.

Safety Stock: An online retailer holds additional inventory to avoid stockouts during peak sales periods.

Buffer Inventory: A pharmaceutical company maintains a surplus of critical medicines to meet unexpected demand or supply disruptions.

Obsolete Inventory: A technology company disposes of outdated smartphones that are no longer in demand.

Packing Materials: A seed company uses sealed bags for seeds as primary packing, boxes for transportation as secondary packing, and shrink wrap for pallets as tertiary packing.

Service Inventory:A café with 10 tables, open 12 hours daily, can serve 120 meals. This capacity is its service inventory.

Book Inventory:Book inventory is the stock shown in records or systems, which may differ from the actual count during physical verification.

Consignment Inventory: A bookstore displays books supplied by publishers on a consignment basis.

Excess Inventory: A retail store ordering more units of a seasonal product than the actual customer demand, leading to unsold items after the season.

Decoupling Inventory: It’s important to have a buffer stock of critical components in a manufacturing plant. This helps prevent disruptions in production, even if the supply chain faces delays.

Theoretical Inventory: To calculate how much raw material is needed for production, look at past demand and production efficiency. Do this without thinking about outside factors.

What Is Inventory Turnover?

Inventory turnover is a financial metric that measures how many times a company sells and replaces its inventory within a specific period (usually a year). It helps businesses evaluate how efficiently they manage stock levels and how well products are selling.

How to Calculate Inventory Turnover:

Average inventory = (Beginning Inventory + Ending Inventory) / 2

Find Average Inventory:

Inventory turnover = Sales + Average Inventory

Understanding Inventory Turnover Ratio

Inventory turnover ratio is a key metric that measures how efficiently a company manages its inventory. It is calculated by dividing the cost of goods sold by the average inventory value during a specific period. A high inventory turnover ratio indicates that a company is effectively selling its inventory and minimizing holding costs. Conversely, a low ratio suggests inefficiency in inventory management and potential issues with overstocking or slow-moving products.

Importance of Inventory Control

Inventory control plays a vital role in optimizing the balance between supply and demand. Effective inventory control helps a company keep the right amount of inventory. This reduces costs and makes customers happier. It involves strategies such as forecasting demand, setting reorder points, implementing safety stock levels, and monitoring stock levels regularly.

By implementing inventory control measures, businesses can achieve several benefits, including:

Cost Reduction: Proper inventory control helps reduce holding costs, such as storage, insurance, and obsolescence expenses.

Improved Cash Flow: Optimized inventory levels prevent excessive investment in inventory, freeing up cash for other business needs.

Enhanced Customer Service: Adequate inventory control ensures products are readily available, leading to improved customer satisfaction and loyalty.

Reduced Stockouts: Efficient inventory control minimizes the risk of stockouts, ensuring that customers' demands are consistently met.

Importance of Inventory Management

Inventory management involves more than just controlling inventory. It takes a comprehensive approach to handling inventory at every stage of its lifecycle. It involves activities such as procurement, storage, tracking, and order fulfillment. Effective inventory management enables businesses to streamline operations, reduce costs, and maximize profitability.

Some key benefits of inventory management include:

Optimized Supply Chain: Good inventory management keeps goods flowing smoothly. It helps avoid disruptions and delays in the supply chain.

Accurate Demand Forecasting: Inventory management allows businesses to accurately forecast demand, enabling proactive planning and production scheduling.

Efficient Resource Allocation: By managing inventory effectively, businesses can allocate resources more efficiently, reducing waste and improving productivity.

Effective Order Fulfillment: Inventory management ensures timely order fulfillment, improving customer satisfaction and reducing order processing time.

What is Inventory Analysis?

Inventory analysis is the process of studying and evaluating inventory data to understand product demand, performance trends, and optimization opportunities. It helps businesses maintain the right stock levels, reduce costs, and forecast future customer needs with greater accuracy.

A key method for inventory analysis is ABC analysis, which classifies products into three groups:

A items: High-demand, fast-moving products that take less space and bring maximum profits (about 20% of inventory).

B items: Moderate-demand products with higher storage costs (around 40% of inventory).

C items: Slow-moving goods that are costly to store and generate the least profit (about 40% of inventory).

ABC analysis is based on the Pareto Principle (80/20 rule), showing that 20% of products often generate 80% of profits. This helps businesses focus on their most valuable items.

In addition, inventory analysis uses metrics such as turnover ratio, stockouts, carrying costs, and lead times to identify inefficiencies. The insights gained guide inventory control strategies like just-in-time (minimizing excess stock) or just-in-case (ensuring availability during uncertainty).

Benefits of Inventory Analysis

Performing regular inventory analysis offers several benefits to businesses, including:

Identifying Slow-Moving or Obsolete Inventory: Inventory analysis helps identify items that are selling slowly or are no longer useful. This allows businesses to take actions like marking them down or disposing of them.

Optimizing Reorder Points: Businesses can look at inventory data and demand patterns. This helps them set the best reorder points, which reduces stockouts and excess inventory.

Improving Forecasting Accuracy: Inventory analysis gives useful information for predicting demand. This helps businesses make better forecasts and avoid having too much or too little stock.

Cost Reduction: Through inventory analysis, businesses can identify cost-saving opportunities such as reducing carrying costs, optimizing storage space, and negotiating better supplier terms.

Improves Cash Flow: By focusing on fast-selling items, businesses avoid tying money in slow-moving stock. This ensures better cash availability for other operations.

Enhances Customer Satisfaction: Understanding customer buying patterns helps businesses keep the right products available, reducing disappointment and boosting loyalty.

Minimizes Project Delays: Analyzing supplier lead times ensures timely reordering, preventing shipment delays and keeping projects on track.

Strengthens Supplier Negotiations: Regular, bulk ordering guided by analysis puts businesses in a stronger position to secure discounts and better pricing from suppliers.

Expands Business Insights: Reviewing inventory data provides a clearer picture of customer preferences, demand trends, and overall business performance.

Inventory Best Practices

Implementing effective inventory management practices can significantly improve operational efficiency and profitability. Here are some best practices to consider:

Regular Inventory Audits: Conduct regular physical inventory audits to ensure accuracy and identify any discrepancies.

Automated Inventory Tracking: Utilize inventory management software to automate tracking, streamline processes, and improve data accuracy.

Demand Forecasting: Implement robust demand forecasting methods to predict future demand accurately and optimize inventory levels.

ABC Analysis: Prioritize inventory based on its value and impact on the business using the ABC analysis method. Focus on managing high-value items more closely.

Collaboration with Suppliers: Build strong relationships with suppliers. This will help ensure timely deliveries, negotiate better terms, and access real-time inventory information.

Cycle Counting Program: A cycle counting program goes beyond routine warehouse operations. By continuously reconciling inventory levels, businesses can ensure data accuracy, reduce discrepancies, and maintain customer satisfaction. This proactive approach minimizes costly stockouts or overstocking, while also saving time and money compared to full-scale physical counts.

Safety Stock (Buffer Stock): Safety stock, often referred to as buffer stock, acts as a safeguard against unexpected demand spikes or supply chain delays. By maintaining a reserve of high-demand or critical materials, companies can prevent production interruptions, avoid missed sales opportunities, and maintain consistent service levels. This backup supply ensures smooth operations even when demand exceeds forecasts.

Batch/Lot Tracking: Batch or lot tracking provides visibility into the lifecycle of products by recording key details about each group of items produced or received. For industries handling perishables, this may include expiration dates or regulatory compliance data. For non-perishable goods, batch tracking helps organizations calculate true landing costs, monitor shelf life, and trace products quickly in the event of recalls or quality issues.

Cloud-Based Inventory Management: Cloud-based inventory management systems allow organizations to monitor stock levels in real time from any location worldwide. Hosted by secure cloud providers, these platforms give companies instant visibility into product availability, SKU locations, and movement across the supply chain. By providing accurate, up-to-date insights, businesses can respond faster to customer needs, streamline operations, and improve overall agility.

Conclusion

Inventory management is a critical aspect of running a successful business. By understanding the various types of inventory, implementing effective inventory control measures, and utilizing inventory analysis, businesses can optimize their operations, reduce costs, and enhance customer satisfaction. By following Dynamic Distributors best practices, businesses can gain a competitive edge. They should also keep checking their inventory performance to stay ahead in today's market.

Related Blogs:

FAQ's Of Inventory

Q: What is the purpose of inventory management?

A: The goal of inventory management is to make sure a company has the right amount of inventory at the right time. This helps reduce costs and increase customer satisfaction.

Q: How often should inventory be counted?

A: The frequency of inventory counting depends on the business's size, complexity, and industry. Small businesses may count inventory annually, while larger businesses may count it more frequently, such as quarterly or monthly.

Q: What is the inventory process?

A: The inventory process includes receiving items, storing them, tracking usage, and moving them into finished products or sales. It is basically the full lifecycle of stock from arrival to customer delivery.

Q: How is inventory controlled?

A: Inventory control means keeping the right amount of stock without overstocking or understocking. Many companies use software to track purchases, sales, storage, and reorders to avoid mistakes.

Q: What is an inventory record?

A: An inventory record shows details about stock on hand, items sold, what’s on order, and where products are stored. Accurate records help control inventory and keep financial reports correct.

Q: What is the average inventory cost?

A: Average inventory cost (also called weighted average cost) is the method of calculating the per-unit cost of goods. Businesses add up the total cost of items and divide it by the number of units. This helps in tracking stock value and pricing decisions.

Q: What are the consequences of overstocking inventory?

A: Overstocking inventory can result in increased holding costs, such as storage expenses and the risk of obsolescence. It uses up money that could be invested in other areas. It might also cause shortages of other products because there isn’t enough storage space.

Q: What are the consequences of understocking inventory?

A: Understocking inventory can lead to stockouts and missed sales opportunities. It can also result in dissatisfied customers and damage to the business's reputation.. It can also result in rush orders, higher costs, and disruptions in the supply chain.

https://gmnc.club/ dạo này thấy mọi người nhắc hoài nên mình cũng bấm vô coi thử cho biết. Không phải kiểu ngồi đọc kỹ từng thứ đâu, mình chỉ xem cảm giác dùng có mượt không thôi. Vừa vào là thấy trang chia khối rõ ràng, nhìn cái là biết khu nào là khu nào, không bị nhồi chữ nên đỡ rối mắt. Mình cũng thích cái kiểu menu đặt ngay chỗ dễ thấy, bấm qua lại nhanh, không cần kéo lên kéo xuống tìm hoài. Mấy chỗ thông tin họ để theo dạng bảng/cột gọn gàng nên lướt trên điện thoại vẫn ổn, không bị tràn hay bé xíu khó đọc. Nói chung nhìn khá “thoáng”, nhất là cách họ…